How Retirement Accounts Are Divided in a Georgia Divorce

When you’re facing divorce in Georgia, one of the most stressful concerns is how your 401K and retirement accounts will be divided. These assets often represent decades of savings and are critical to your future financial stability. Because retirement accounts are governed by both state divorce law and complex federal rules, confusion and costly mistakes are common without clear guidance.

In this guide, we will walk through how Georgia courts determine what portion of a retirement account is marital property, how equitable distribution actually works in practice, and what legal tools, including QDROs, are required to divide these assets without unnecessary taxes or penalties. Understanding Georgia’s laws on dividing retirement accounts can help you prepare strategically, protect what is rightfully yours, and make informed decisions about your long-term financial future.

Equitable Distribution: What “Fair” Really Means

Georgia follows an equitable distribution system, meaning assets are divided fairly – but not necessarily equally. The court reviews factors such as:

- Length of the marriage

- Each spouse’s financial and non-financial contributions

- Current and future income potential

- Health, age, and post-divorce financial needs

The goal is to ensure both spouses can maintain financial stability after the divorce. With that framework in mind, the next step is understanding exactly which portions of a retirement account are considered marital property and which may remain separate under Georgia law.

What Counts as Marital vs. Separate Property in Georgia

In Georgia, the portion of your 401K, pension, or IRA earned during your marriage is considered marital property. That means it’s subject to equitable division, even if the account is solely in your name.

However, contributions and growth before the marriage usually remain your separate property. Tracing and documenting those pre-marital funds is key to ensuring they’re excluded from division.

How a 401K in a Divorce Is Divided, Including Pensions and Other Retirement Plans

In a Georgia divorce, dividing a 401K, pension, or other employer-sponsored retirement plan typically requires a Qualified Domestic Relations Order (QDRO). This legal document allows a portion of one spouse’s retirement benefits to be transferred to the other without tax penalties or early withdrawal fees.

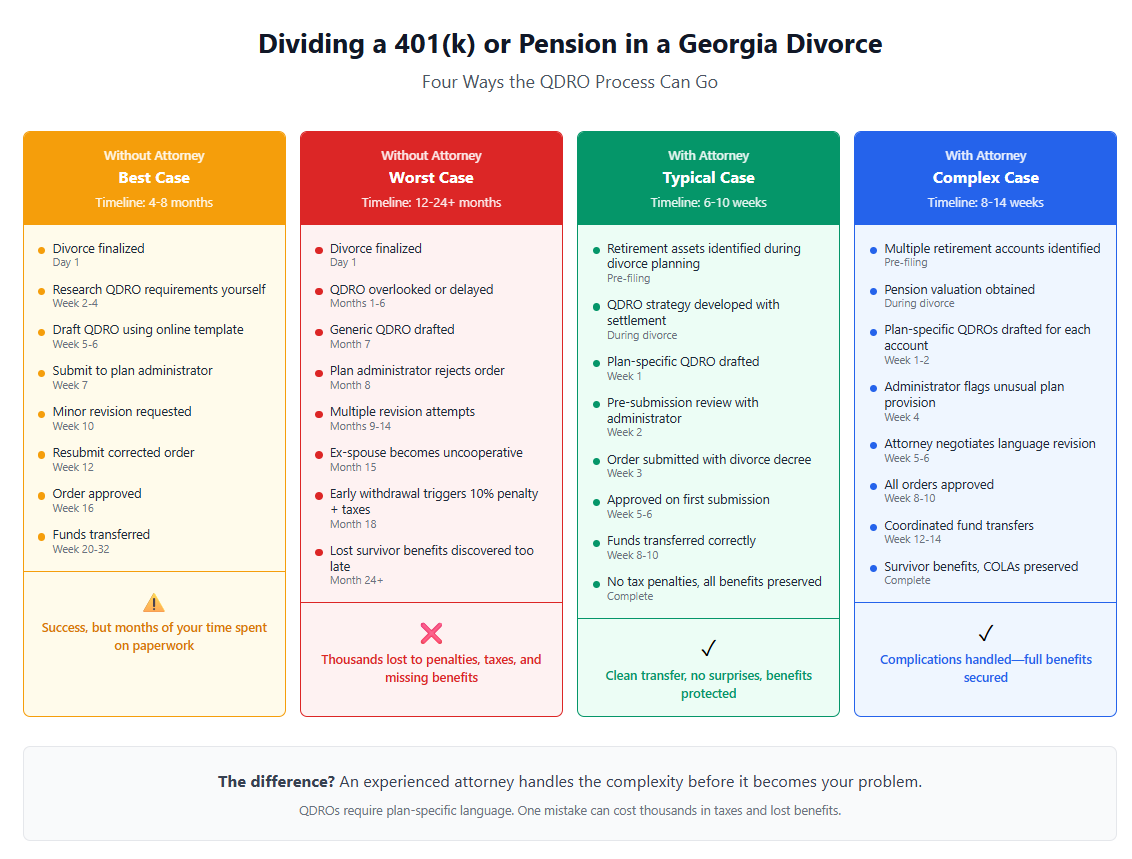

Dividing a 401K or pension is rarely a single-step process, and where things break down is usually between the divorce order and the retirement plan itself. Understanding how that process flows, and where problems commonly arise, helps explain why attorney involvement matters.

Below is a simplified visual walkthrough of how retirement division typically unfolds, showing where delays, rejections, and tax problems commonly occur, compared side by side with how the process looks when handled by an attorney at Hastings Shadmehry Family Law.

Tax and Timing Considerations

Mistakes in dividing retirement assets can be costly, and in many cases, the financial impact is not immediately obvious. Small oversights made during a divorce can result in significant tax exposure, lost retirement growth, or benefits that cannot be recovered later. Common errors include:

- Withdrawing funds instead of using a QDRO, triggering taxes and penalties.

- Ignoring future growth, failing to specify whether post-divorce contributions count.

- Misvaluing pensions, not considering present value or survivor benefits.

At Hastings Shadmehry Family Law, we work directly with financial professionals when needed to accurately value retirement accounts, assess tax exposure, and structure divisions that protect your long-term interests, not just the numbers on paper. In some cases, however, retirement assets are governed by additional federal rules that go beyond standard private accounts, which is why military and government retirement plans require separate consideration.

Dividing Military or Government Retirement Accounts

If one or both spouses served in the military or are government employees, special rules apply, and these accounts often cannot be divided the same way as a private-sector 401K. Federal laws like the Uniformed Services Former Spouses’ Protection Act (USFSPA), along with agency-specific pension systems for federal and state employees, impose strict requirements on how benefits may be awarded, calculated, and paid.

These plans may limit when payments begin, how survivor benefits are handled, or whether cost-of-living adjustments are shared, making careful drafting and long-term planning essential. Proper handling ensures benefits are divided correctly, complies with federal regulations, and avoids delays or unintended reductions in future payments. With these added complexities in mind, the focus then shifts to protecting your overall retirement picture and making sure today’s divorce decisions support your financial security long after the case is finalized.

Protecting Your Retirement Future

Divorce doesn’t have to derail your retirement plans. With the right legal strategy, you can preserve your share of retirement savings and plan confidently for your financial future. A knowledgeable attorney will:

- Determine which assets are marital vs. separate

- Draft or review QDROs and similar orders

- Negotiate fair settlements based on total marital assets

- Protect your rights in mediation or court

Get Guidance from a Trusted Georgia Divorce Attorney

At Hastings Shadmehry Family Law, we understand that your retirement represents years of hard work. Our legal team helps clients throughout Georgia divide 401Ks, pensions, and other retirement assets fairly and efficiently, so you can move forward with peace of mind.